You pay your premium every month. You assume you're covered. Then you file a claim and hear the worst three words in insurance: "Claim denied -- policy violation."

Most people don't realize that dozens of everyday situations can give your insurer grounds to reduce, deny, or outright void your coverage. Here are 7 of the most common -- and most of them are things people do without thinking twice.

High Risk

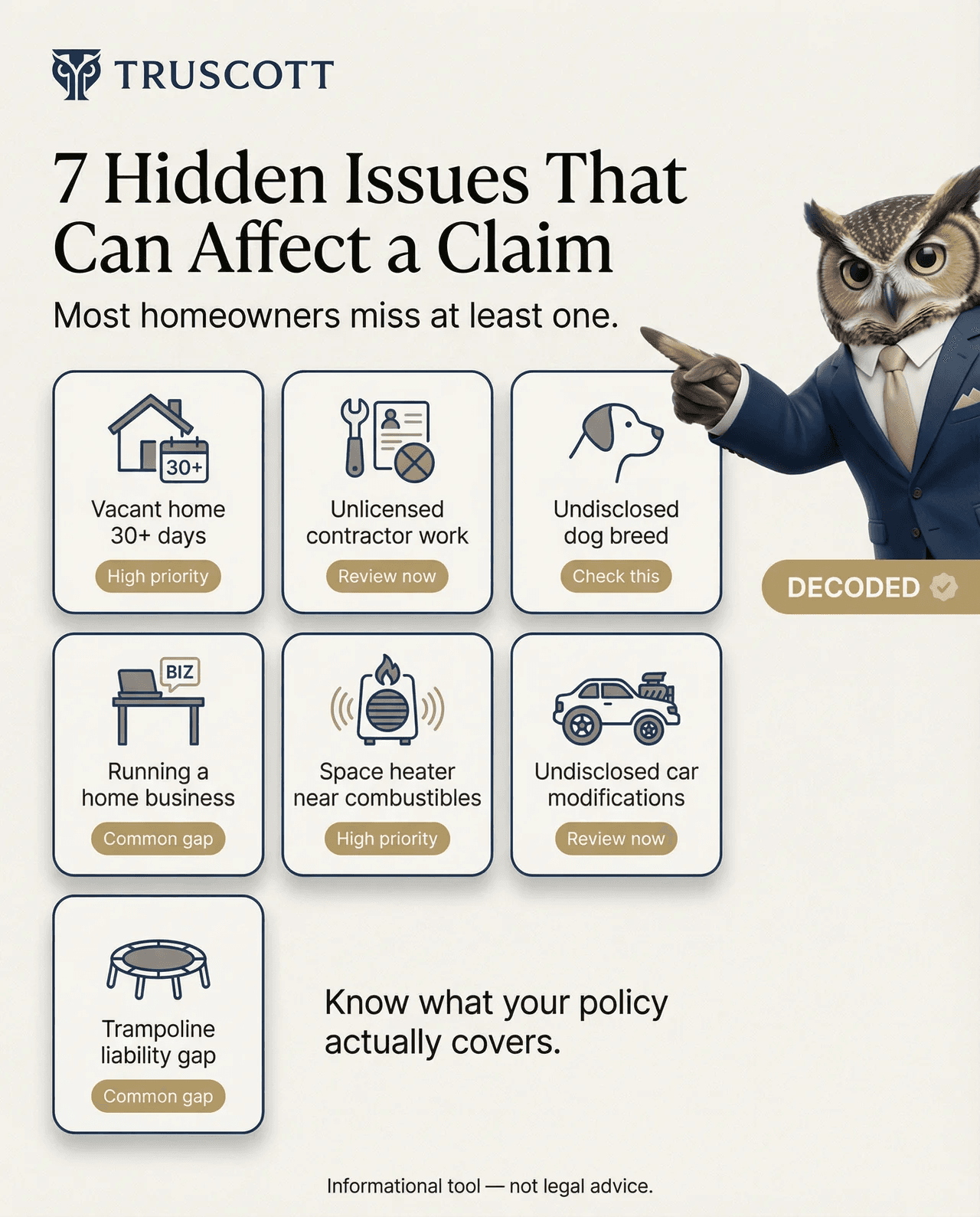

1. Leaving Your Home Vacant for 30+ Days

Going on an extended vacation, snowbirding for the winter, or leaving a property empty while it's on the market? Most homeowners policies have a vacancy clause that kicks in after 30 consecutive days. Once triggered, your insurer can deny claims for vandalism, theft, water damage, and more. Some policies void coverage entirely. The reasoning: empty homes are higher risk for undetected damage and break-ins.

High Risk

2. DIY Renovations Without Permits

That bathroom you gutted and rebuilt yourself? If the work required a building permit and you didn't pull one, your insurer has grounds to deny any claim related to that work. A pipe bursts in your new bathroom and floods the house? They can argue the damage resulted from unpermitted work and refuse to pay. It doesn't matter that the pipe burst had nothing to do with the renovation -- the unpermitted work gives them an out.

Medium Risk

3. Owning a 'Restricted' Dog Breed

Pit bulls, Rottweilers, German Shepherds, Dobermans, Chow Chows, Akitas, and wolf hybrids are on many insurers' restricted breed lists. If you own one and didn't disclose it, your entire homeowners policy could be voided -- not just the liability portion. Insurers argue that failing to disclose a restricted breed is material misrepresentation on your application. One dog bite claim can expose the non-disclosure and unravel your entire policy retroactively.

Medium Risk

4. Running a Business From Home Without Telling Your Insurer

If clients visit your home, you store business inventory in your garage, or you use your home as a base for a contracting or delivery business, your homeowners policy likely doesn't cover it. A client trips on your front steps? Your homeowners liability might deny the claim because it was a business visitor. Inventory gets stolen? Business property usually isn't covered under personal property limits. The home-based business exception that people assume exists... mostly doesn't.

High Risk

5. Neglecting Maintenance Until Something Breaks

Insurance covers sudden, accidental damage -- not gradual deterioration. If your roof is 25 years old and finally gives way, your insurer will argue it was a maintenance issue, not a covered peril. A tree root that slowly cracked your foundation over 5 years? Maintenance. A furnace that failed because you never serviced it? Maintenance. Mold that grew because you ignored a small leak? Maintenance. The line between "sudden damage" and "you should have fixed this" is wherever your insurer draws it.

Medium Risk

6. Having a Trampoline, Pool, or Tree House Without Disclosing It

These are called "attractive nuisances" in insurance-speak -- things that attract children and increase your liability risk. Many insurers require specific disclosure and may require additional liability coverage, fencing, or safety measures. If you install a trampoline and don't tell your insurer, and a neighborhood kid gets hurt on it, your insurer can deny the liability claim for non-disclosure. Some insurers won't cover you at all if you have a trampoline, regardless of fencing or nets.

Low Risk

7. Renting Out Your Home on Airbnb Without a Rental Endorsement

Your standard homeowners policy almost certainly excludes short-term rental activity. If a guest gets hurt, if they damage your property, or if a fire breaks out while they're staying -- you're likely not covered. Airbnb's Host Protection Insurance has significant exclusions and deductibles that most hosts never read. And if your insurer discovers you've been renting without disclosure, they can cancel your entire policy, not just deny the rental-related claim.

Policy Risk Scorecard

Answer honestly -- do any of these apply to you right now?

Is your home (or a second property) ever vacant for 30+ consecutive days?

Have you done any renovation work without building permits?

Do you own a dog breed that might be on an insurer's restricted list?

Do you run any kind of business from your home?

Have you skipped annual maintenance on your roof, HVAC, or plumbing?

Do you have a pool, trampoline, or tree house that you haven't disclosed?

Have you rented your home on Airbnb, VRBO, or similar without a rental endorsement?

The Common Thread

Every single one of these violations comes down to the same thing: what your insurer doesn't know can hurt you. Insurance is a contract based on disclosure. When the facts on the ground don't match what's in your policy, the insurer holds the leverage.

The fix is straightforward: read your policy, disclose changes, and ask questions before you need to file a claim. Five minutes of honesty with your agent today can save you from a six-figure denial tomorrow.

Start with your policy

Upload your policy to Truscott and we'll flag exclusions, disclosure requirements, and coverage conditions in plain English. Most people are surprised by what's actually in their policy -- and what isn't.

The Real Insurance Rule

Insurance doesn't work like a safety net that catches you no matter what. It works like a contract -- and contracts have conditions. The conditions are buried in 40 pages of fine print that nobody reads.

Your insurer read every word. Shouldn't you?