Most people don't read their insurance policy until something goes wrong. By then, it's too late. Here are five gaps that catch people off guard every single day -- and what you can do about them.

1. Your "Full Coverage" Auto Policy Probably Isn't Full

That phrase gets thrown around a lot, but there's no official definition of "full coverage." Most of the time it just means liability plus collision and comprehensive. It almost never includes gap coverage, rental reimbursement, or rideshare protection. If you're still paying off your car and it gets totaled, you could owe thousands more than the payout.

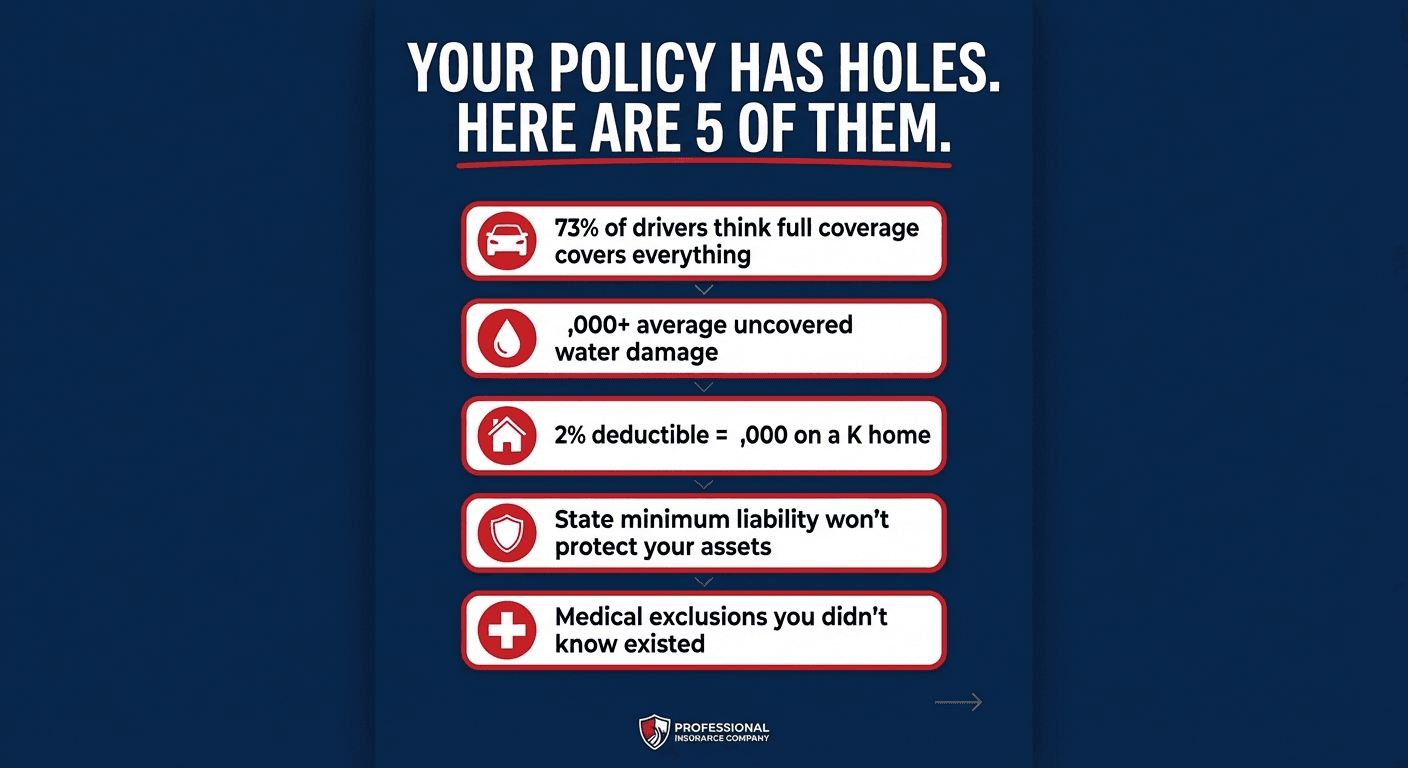

73%of drivers think "full coverage" covers everything

2. Your Homeowners Policy Has a Water Damage Blind Spot

Standard homeowners insurance typically covers sudden water damage -- like a burst pipe. But gradual leaks, sewer backups, and flood damage? Those are usually excluded entirely. People find this out the hard way when their basement floods after a storm.

$10,000+average cost of water damage not covered by standard policies

3. Your Deductible Might Be Higher Than You Think

Many people set a high deductible years ago to lower their premium, then forget about it. If your deductible is $2,500 and the repair costs $3,000, your insurance is only covering $500. For wind and hail damage, some policies use a percentage-based deductible (like 2% of your home's insured value), which can be significantly more than a flat dollar amount.

2%of home value = $8,000 deductible on a $400K home

4. Your Liability Limits Might Not Protect Your Assets

The minimum liability coverage required by your state is designed to keep you legal -- not to keep you financially safe. If you cause an accident and the damages exceed your policy limits, you're personally responsible for the difference. That means your savings, your home, and your future earnings are on the line.

$200/yrfor $1 million in umbrella coverage

5. Your Life Insurance Might Not Cover What You Think

Term life is straightforward, but many whole life and universal life policies have fine print around loans, lapses, and cash value that can reduce your death benefit. If you've borrowed against the policy or missed premium payments, your beneficiaries might receive far less than expected.

40%of life insurance policyholders don't know their exact death benefit

Quick Coverage Gap Check

Answer 5 questions to see how exposed you might be.

Do you know exactly what your auto policy covers beyond "full coverage"?

Does your homeowners policy include sewer/drain backup coverage?

Can you comfortably pay your current deductible out of pocket today?

Are your liability limits higher than your total assets (home equity, savings, investments)?

Have you checked your life insurance death benefit in the last 12 months?

The 60-Second Fix

You don't need to become an insurance expert. You just need to actually look at what you're paying for. Upload any policy to Truscott and get a plain-English breakdown of your coverage, gaps, and exclusions -- free, in about a minute.

Your insurance company wrote that policy to protect themselves. We built Truscott to protect you.