Here's a number that should make every homeowner uncomfortable: roughly 80% of American homes are underinsured, many by 20% or more. That means if your house burned down tomorrow, your insurance payout wouldn't cover the cost to rebuild it.

The gap between what your policy covers and what it actually costs to rebuild has been growing quietly for years. Here's why it happens, how to check, and what to do about it.

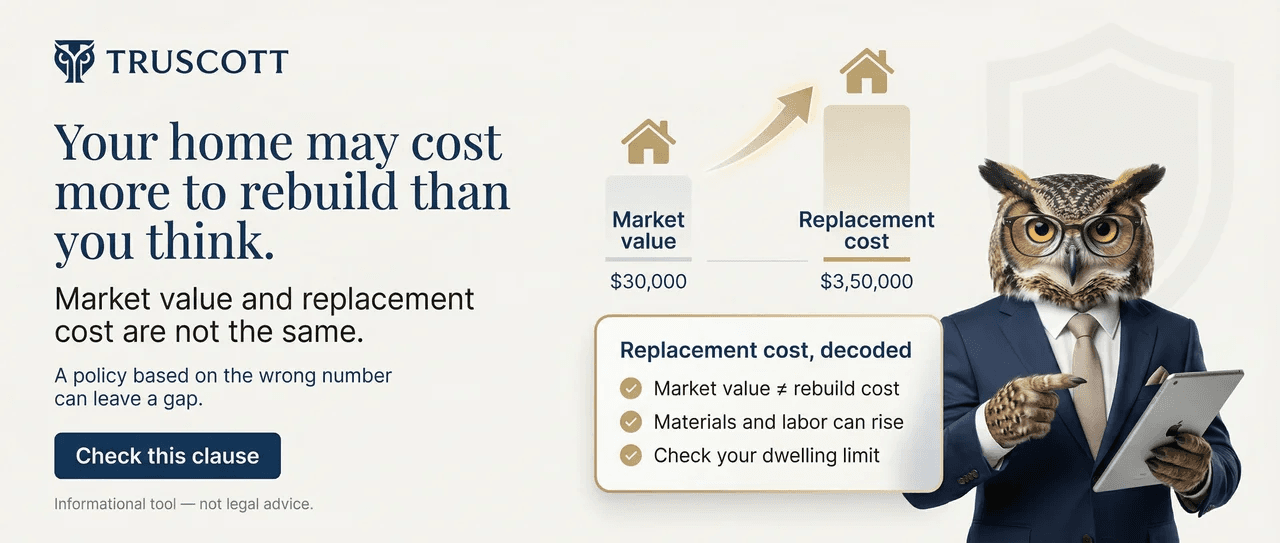

Construction Costs Have Exploded

Between 2020 and 2025, residential construction costs rose 30-40% nationwide. Lumber, labor, concrete, roofing -- everything costs more. Your home might be worth $400,000 on Zillow, but rebuilding it from scratch could cost $550,000 or more. Your insurance policy doesn't track the real estate market. If you haven't updated your dwelling coverage, you're covered for what it would have cost to rebuild years ago, not today.

35%average construction cost increase since 2020

Renovations Silently Widen the Gap

That kitchen remodel you did in 2022? The finished basement? The new deck? Every improvement increases your home's replacement cost. But unless you called your agent after each project, your dwelling coverage hasn't budged. A $60,000 kitchen renovation means your rebuild cost is $60,000 higher. If your coverage didn't go up by $60,000, you just created a gap.

$60Kaverage kitchen remodel cost -- rarely added to policies

The 80% Rule Will Cost You Even More

Most insurance policies have an 80% coinsurance clause. It means you must insure your home for at least 80% of its replacement cost, or the insurer will penalize you on every claim -- even partial ones. If your home costs $500,000 to rebuild and you're only covered for $350,000 (70%), your insurer can reduce your payout proportionally. A $50,000 kitchen fire claim? They'd only pay $43,750. You'd eat the rest plus your deductible.

80%coinsurance threshold -- fall below it and every claim is penalized

Your Insurer's 'Guaranteed Replacement' Isn't What You Think

Some policies advertise "guaranteed replacement cost" coverage. Sounds bulletproof, right? Read the fine print. Many of these policies cap the guaranteed replacement at 125% or 150% of your dwelling coverage. If your dwelling coverage is already low, 125% of an inadequate number is still inadequate. And in a widespread disaster -- hurricane, wildfire -- construction costs spike even higher due to demand. That 125% cap disappears fast.

125%typical cap on 'guaranteed' replacement -- not unlimited

Am I Underinsured?

Enter your numbers to see whether your coverage keeps up with today's rebuild costs.

$300,000

2018

$300,000

Renovation Coverage Check

Home improvements increase your rebuild cost. Has your policy kept up?

Have you renovated your kitchen or bathrooms in the last 5 years?

Have you added a deck, patio, pool, or finished basement?

Has your insurer done a replacement cost review in the last 2 years?

Do you have an inflation guard endorsement on your policy?

Do you know the difference between market value and replacement cost?

How to Close the Gap

The 60-Second Reality Check

You don't need to hire an appraiser to find out if you're underinsured. Upload your policy to Truscott and we'll show you your dwelling coverage limit, flag potential gaps, and explain what your coinsurance clause means in plain English.

80% of homeowners are underinsured. The question isn't whether the odds are against you -- it's whether you're willing to check.