Somewhere in a filing cabinet or email thread, there's an insurance declarations page with your name on it. On that page is a number you probably picked years ago and haven't thought about since.

That number is your deductible. And for millions of homeowners, it's a ticking time bomb.

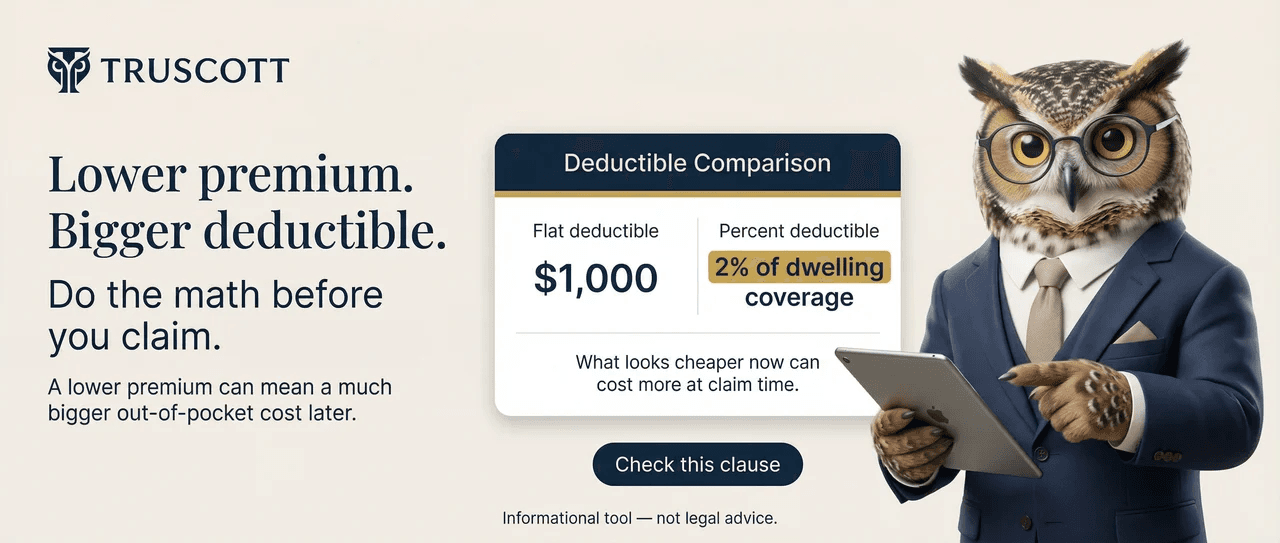

The $100 Decision That Snowballed

Here's how it usually goes: When you bought your home, your agent asked what deductible you wanted. You picked a higher one to save $100 or $150 a year on your premium. At the time, the math made sense. You were thinking about monthly payments, not disasters.

Fast forward a few years. Your home has appreciated. Maybe you refinanced. Your coverage limits went up accordingly. But your deductible? It quietly changed from a flat dollar amount to a percentage of your insured value.

The math most homeowners never do:

$400K home, 2% deductible:$8,000

$600K home, 2% deductible:$12,000

$400K home, 5% hurricane:$20,000

$600K home, 5% hurricane:$30,000

Deductible Impact Calculator

Enter your home's insured value to see what you'd actually pay out of pocket with different deductible types.

$400,000

$100K$1.5M

The Hurricane Deductible Trap

If you live in a coastal or hurricane-prone state (Florida, Texas, Louisiana, the Carolinas, and others), you likely have a separate hurricane or wind/hail deductible. This is almost always percentage-based, ranging from 2% to 10% of your dwelling coverage.

A 5% hurricane deductible on a $500,000 home means you're responsible for the first $25,000 of hurricane damage. That's not a deductible -- that's a second mortgage.

The Liability Blind Spot

Your deductible isn't the only number hiding on your declarations page. Your liability limit might be equally dangerous. Most standard homeowners policies come with $100,000 or $300,000 in liability coverage. If someone gets seriously injured on your property and sues, those limits evaporate fast.

Medical bills, legal fees, and lost wages can easily exceed $300K. The difference comes out of your savings, your home equity, and potentially your future earnings.

Liability Gap Analyzer

Compare your total assets against your liability coverage to see if you're exposed.

$500,000

$300,000

CoverageTotal assets

GAP: $200,000

You have a $200,000 liability gap.

If you're sued and damages exceed your coverage, your personal assets are on the line. A $1M umbrella policy typically costs $200-$300/year.

What You Can Do Right Now

The Real Cost of Not Looking

That $100 you saved years ago on a higher deductible? It could cost you $8,000, $20,000, or more when you actually need your insurance. The 60 seconds it takes to upload your policy to Truscott could be the most valuable minute you spend this year.

Your insurance company is counting on you not reading the fine print. Don't let them be right.