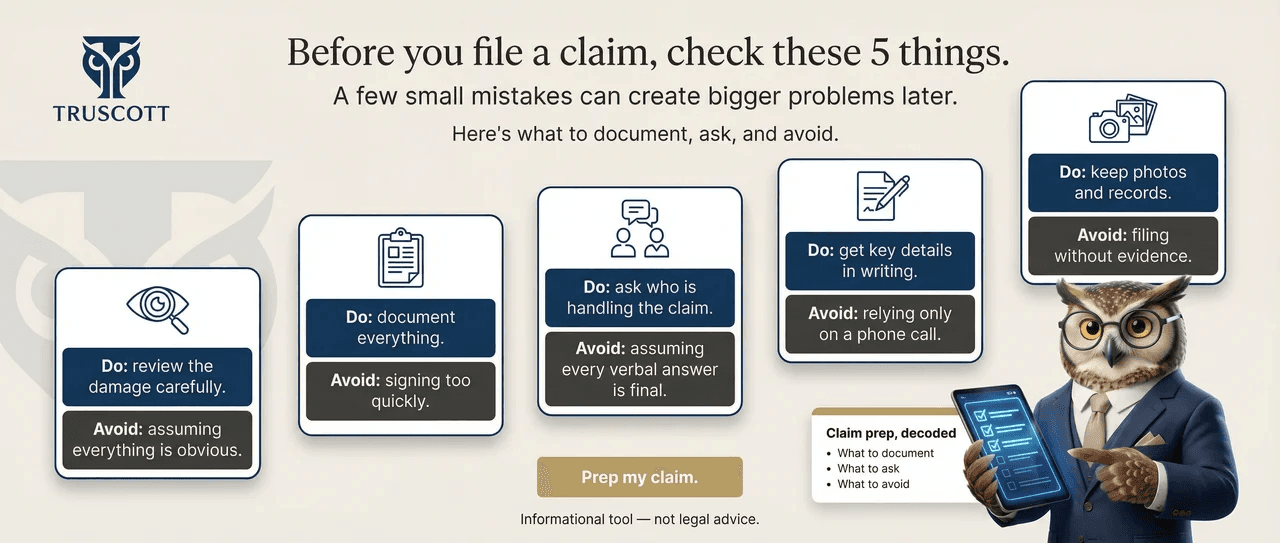

The claims process is designed to protect the insurer, not you. Every step -- from the first phone call to the final settlement -- is structured to minimize what they pay out.

That doesn't mean they're breaking the law. It means they have a system, and you don't. Until now. Here are five things your insurance company won't volunteer -- and how to use them to your advantage.

1. They'll Ask for a Recorded Statement -- You Don't Have to Give One Immediately

Within hours of filing a claim, an adjuster will call and ask to take a recorded statement. They'll make it sound routine. It is routine -- for them. But you're under no legal obligation to give one on the spot. Anything you say can be used to minimize or deny your claim. Adjusters are trained to ask leading questions that can trip you up when you're stressed and still assessing the damage.

2. Their First Offer Is Almost Never Their Best Offer

Insurance companies budget for negotiation. The first settlement offer is typically the lowest amount they think you'll accept. Studies show that claimants who negotiate receive 20-40% more than the initial offer on average. The adjuster knows this. They're counting on you not knowing it.

3. Depreciation Is Their Favorite Tool -- and It's Negotiable

On most claims, the insurer calculates depreciation on your damaged items. A 5-year-old roof? They'll pay you for a 5-year-old roof, not a new one -- even though you can't buy a used roof. What they won't tell you: if you have replacement cost coverage (check your declarations page), you're entitled to the full replacement amount once repairs are completed. Many people accept the depreciated check and never claim the rest.

4. You Can Hire Your Own Adjuster -- and They Can't Stop You

The adjuster who shows up works for the insurance company, not you. Their job is to assess damage conservatively. You have the right to hire a public adjuster who works on your behalf, typically for 10-15% of the settlement. On claims over $10,000, a public adjuster often recovers significantly more than their fee. Insurance companies rarely mention this option.

5. A Denied Claim Isn't the End -- It's an Opening

About 1 in 5 homeowners insurance claims gets denied on the first attempt. But a denial letter isn't a verdict -- it's a starting position. You have the right to appeal, request a re-inspection, and escalate to your state's Department of Insurance. The three most powerful words in insurance disputes: "I'd like to escalate." The moment you mention regulatory oversight, the tone of the conversation changes.

Claims Readiness Checklist

0/8Do these before you call the adjuster.

The Bottom Line

Your insurance company has professional adjusters, legal teams, and decades of claims data working for them. You deserve to walk in with more than a prayer and a phone number.

Upload your policy to Truscott before your next claim. Know exactly what you're covered for, what your deductible is, and what to say when the adjuster calls. It takes 60 seconds and it's free.